Property investors can also use their superannuation to purchase property (both residential or commercial). Here, property investors will need to set up their own ‘self-managed’ super fund. This allows investors more control to direct their super into specific assets of their own choosing.

Since 2007, the Australian government has allowed property investors to leverage funds held inside their superannuation. This has sparked a surge in ‘mum and dad’ property investors using super, who previously did not have enough funds available inside super to buy properties outright.

To protect the superannuation system from losses, the government did put in place a strict set of borrowing rules. For example, SMSF property assets cannot be used for personal purposes. In addition, there is no scope to develop or improve property assets held inside an SMSF. This means strategies like renovating or developing are not possible.

SMSF lending is reasonably new and is one of the fastest growing areas of lending. However, in more recent times, there has been some scale back of SMSF loans in the marketplace, with many lenders introducing greater restrictions and higher pricing to their SMSF loan products.

Property spruikers often target SMSF investors to sell poor property investments.

Properties being purchased inside and SMSF should be put under the same rigorous due diligence testing as any investment.

Given the rules, asset selection may vary slightly in favour of newer dwellings that don’t need improvements. Income producing investments that are more self-sustaining (not negative gearing based strategies) are also commonly favoured given the limited contributions made (10% of salary).

Why is it attractive:

- It allows investors to leverage their funds held inside super. This means fund balances of ~$250,000 can be turned into nearly $1,000,000 in total assets. This means that SMSF property investing allows greater ‘risk taking’ than otherwise. Superannuation is usually quite conservative, leveraging offers scope to take more risk and potentially earn higher returns.

- Other super assets (e.g. shares, cash, etc) are quarantined and protected from any potential property losses. This is to ensure that borrowing through your SMSF does not place other retirement investments held in your SMSF at risk.

- Legislation requires that the loan must be under a limited recourse borrowing arrangements. This facility allows the lender to hold the property as security however any existing or other assets held by the SMSF cannot be used for additional security. Subsequently the lender may insist that the members provide personal guarantees (disadvantage).

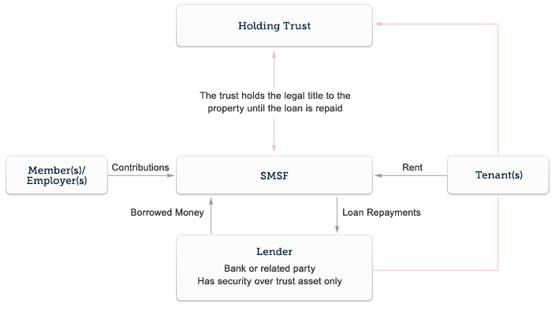

- The way this works in practise is that the asset that is purchased under a borrowing arrangement must be held in a specific holding trust until the loan is repaid. Further, the only SMSF asset that can be used as security for this loan is the asset that is held within this trust – hence the name Limited Recourse Borrowing Arrangements – which helps to protect other assets held inside your SMSF.

Why is it unattractive:

- Compliance costs – running an SMSF is expensive and involves annual audits, tax returns, more paperwork. Setting up the above structure also involves fees. This complexity adds about $2,000 in running costs a year.

- Restricts borrowing power to continue purchasing – lenders require you to provide a personal guarantee that you will personally cover the loss in the event of default (as other SMSF assets are not available as security). This personal guarantee can reduce your borrowing power with some lenders who will factor in the potential repayments in your serviceability testing. This is commonly the case with larger institutions. It therefore makes sense to begin investing with super funds once your personal investing is complete.

- No equity releases – legislation restricts the ability to release equity created in the investments.

- May need to diversify some assets away from property – having all your investments in property may not be prudent. Superannuation is usually a good way to have exposure to shares and other investment vehicles.

- Complexity of documentation – obtaining loan approvals is more complex, there are guarantor loan contracts to be signed (more complex) and this usually involves obtaining financial and legal advice from professionals.

COMMENTS