Income treatment is quite similar between individual lenders. Different types of income are treated differently. Generally, the more stable the income, the more the banks will include of it. The longer the history you can show, the greater the chance all of it can be used in lender serviceability calculations.

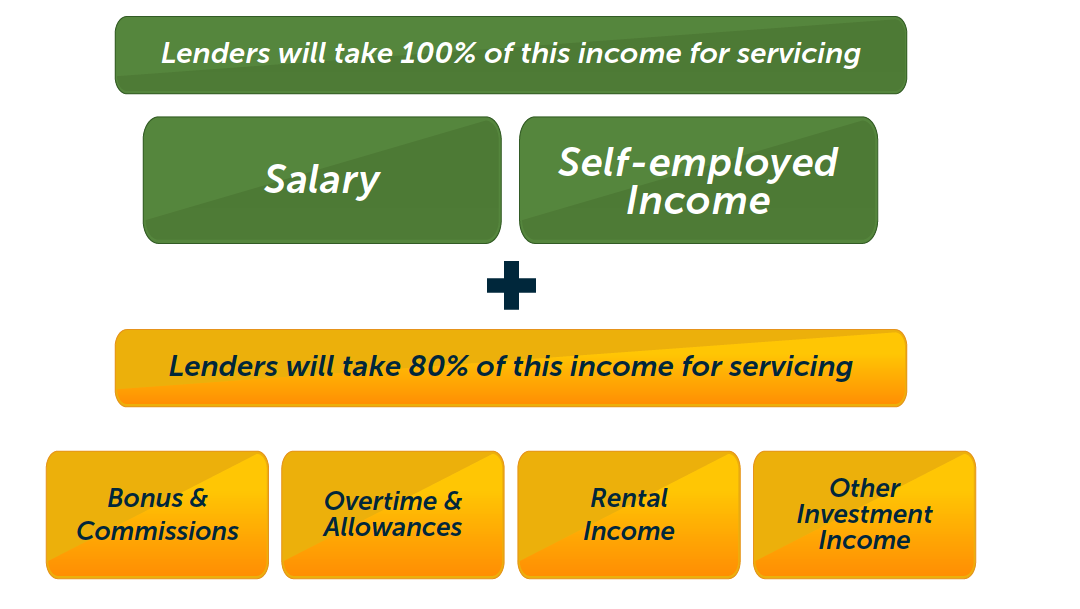

- Salary: lenders will usually allow 100% of your salary income to be included in their serviceability metrics. They will of course apply standard tax rates and use your net income, as this is what’s available to you to repay the loan every month. Compulsory superannuation payments are excluded from servicing calculators.

- Different types of employment may be treated differently. As a general guide, banks will either include all your salary income or none of it. For example, with some lenders you need a 6-12 month history of employment in your role. Without this, they won’t include any of your income in their calculations and you won’t be able to borrow. Conversely, there are lenders that will accept your employment income from day 1.

- Salaried income that involves variable rates of income, like seasonal employment and casual employment, usually need longer histories to be demonstrated. Nonetheless, some lenders allow three months’ history while others require twelve.

- Overtime & allowances: lenders usually allow 80% of overtime income to be included in serviceability assessments. This is because overtime is considered more variable/uncertain, hence this income is partly shaded in serviceability calculations. With some lenders, allowances are included at 100% as they are typically part of borrower’s remuneration package.

- Bonuses, commissions: Lenders allow 80% of bonus and commissions income to be included. Usually you require 12 month history for commission income and 2 years history to evidence bonus payments.

- Profits/self-employed: For those that are self-employed, lenders examine the business’s net income (profit) to determine serviceability. If you’ve paid yourself a salary, they add this back to the profit figure and use 100% of the net income. Most lenders require two years tax returns to evidence this income, but some lenders like CBA, Westpac & ANZ can use the latest year only.

- Lenders will also ‘addback’ certain expenses to your profit figure and include this in your income. These include depreciation expenses, interest charges on loans already expensed, and additional superannuation payments made beyond compulsory payments.

- Rental income: Lenders usually include 80% of any rental income earned. Lenders will include the future rental income that is about to be earned if purchasing an investment property.

- Other investment income: Investment income in the form of dividends, distributions, etc may be included. These are usually included at 80% of their true value, and requires 2 years tax return evidence to be included in serviceability assessments.

COMMENTS